Bank executives told The Australian Financial Review the worst case scenario was extreme and difficult to model given the short weekend deadline. “We think that's probably part of the test,” said one senior banker. “If you can't do this modelling or say you're not sure of the impact, APRA will be onto it.”

The banks have already done this modelling, of course.

The rest of the article just spells out how little the banks have had to worry about previously, and not much now.

Australia's banks have limited exposure to Europe, totalling $87.2 billion, or 2.7 per cent of assets, according to the RBA. Of that amount, $74.6 billion is exposed to borrowers in core nations – France Germany and the Netherlands – mostly to banks.

All this worst case scenario testing is exactly why Australian banks are where they are.

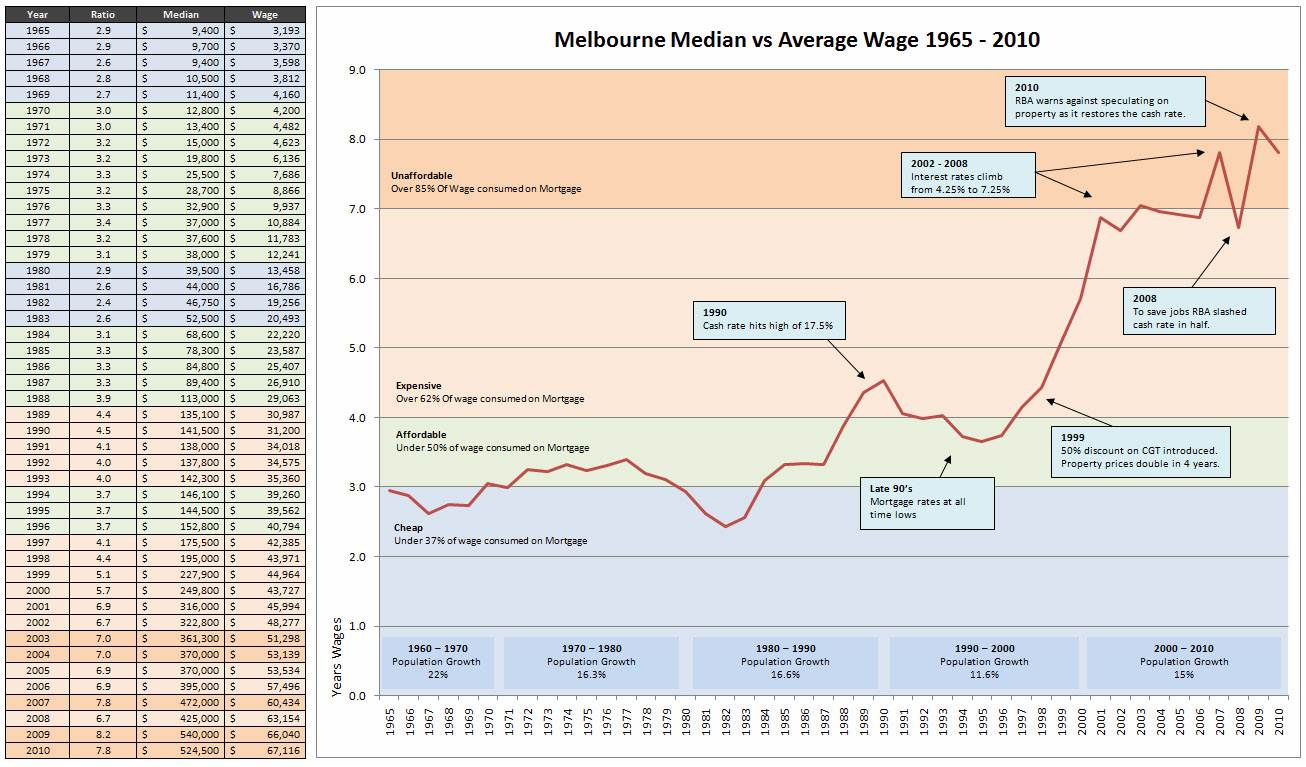

As for THE GREAT HOUSE PRICE CRASH - It's nearly 2012, waiting for the crash is like waiting for Jesus to return